AUTUMN GENERAL MEETING PDF Free Download

1 / 115/115

100%

AUTUMN GENERAL

MEETING

8 SEPTEMBER 2025

WELCOME

Rebecca Brooks

Chair

AGENDA

1. Review of Minutes – Emma Gordon, Board Director

2. Association Update – Joss Croft OBE, CEO

3. Headwinds and Tailwinds – David Edwards, Scattered Clouds

4. Q&A

REVIEW OF

MINUTES

Emma Gordon

Board Director

ASSOCIATION

UPDATE

Joss Croft

CEO

MAXIMISING YOUR MEMBERSHIP

Talk to us about your business

Come along to the events

Utilise our marketing services

Host an event or suggest a webinar topic

Engage with each other

9

WHAT HAVE WE BEEN UP TO? EVENTS

11

EVENTS TEAM APPOINTMENT

12

UKINBOUND INSPIRE 2025

WHAT HAVE WE BEEN UP TO? ADVOCACY

WHAT HAVE WE BEEN UP TO? MEDIA

25 pieces of coverage

Over 1 million total reach

WHAT HAVE WE BEEN UP TO? MARCOMMS

WHAT HAVE WE BEEN UP TO? MARCOMMS

WHAT’S NEXT

•Membership renewals

•Business Barometer

•IFTM Top Resa: 23 – 25 September

•World Travel Market London: 5 – 7 November

•National Sales Conference: 13 November

•Use discount code UKINBMEMBER

•Britain & Ireland Marketplace:

•Use discount code 26UKIBIM

•Annual Convention 2026: bookings opening soon

Inbound tourism: the tailwinds and headwinds

David Edwards

September 2025

Context

Foreign bednights spent in Europe: 2014=100

Outbound travel from all world regions is forecast to grow this year and next

Intentions of Europeans to travel within Europe during next six months

Main challenges facing international tourism according to UNWTO Panel of Experts

Britain is being outcompeted in attracting inbound visitors (growth in period 1995-2024)

European destinations reporting inbound arrivals growth in first half of 2025

Across all countries to have reported

January to June figures to Tourmis

aggregate year-to-date growth in

foreign visitor arrivals stands at 5.1%

Inbound trends

Arrivals at the UK border – rolling 12-month tally

In the first half of 2025 the number of British National

arrivals is 7.2% up on the same period of last year, while

the number of Other Nationality arrivals is up just 0.6%

Visitor visas issued – rolling 12-month tally

In the first half of 2025 the number

of visitor visas issued was 5% up

on the same period of last year

Number of ETAs issued up to June 2025

Inbound volume and value trends 1980-2024

Volume remains 2% below 2019

and spend 8% down in real terms

Average spend per visit 1980-2024 (constant prices)

The amount that the typical inbound visit generates is now one-

third lower in real terms than had been the case in the mid 1980s

Average length of stay (nights) 1980-2024

The decline in spend per visit is due to

length of stay having fallen by around

one-third across the past four decades

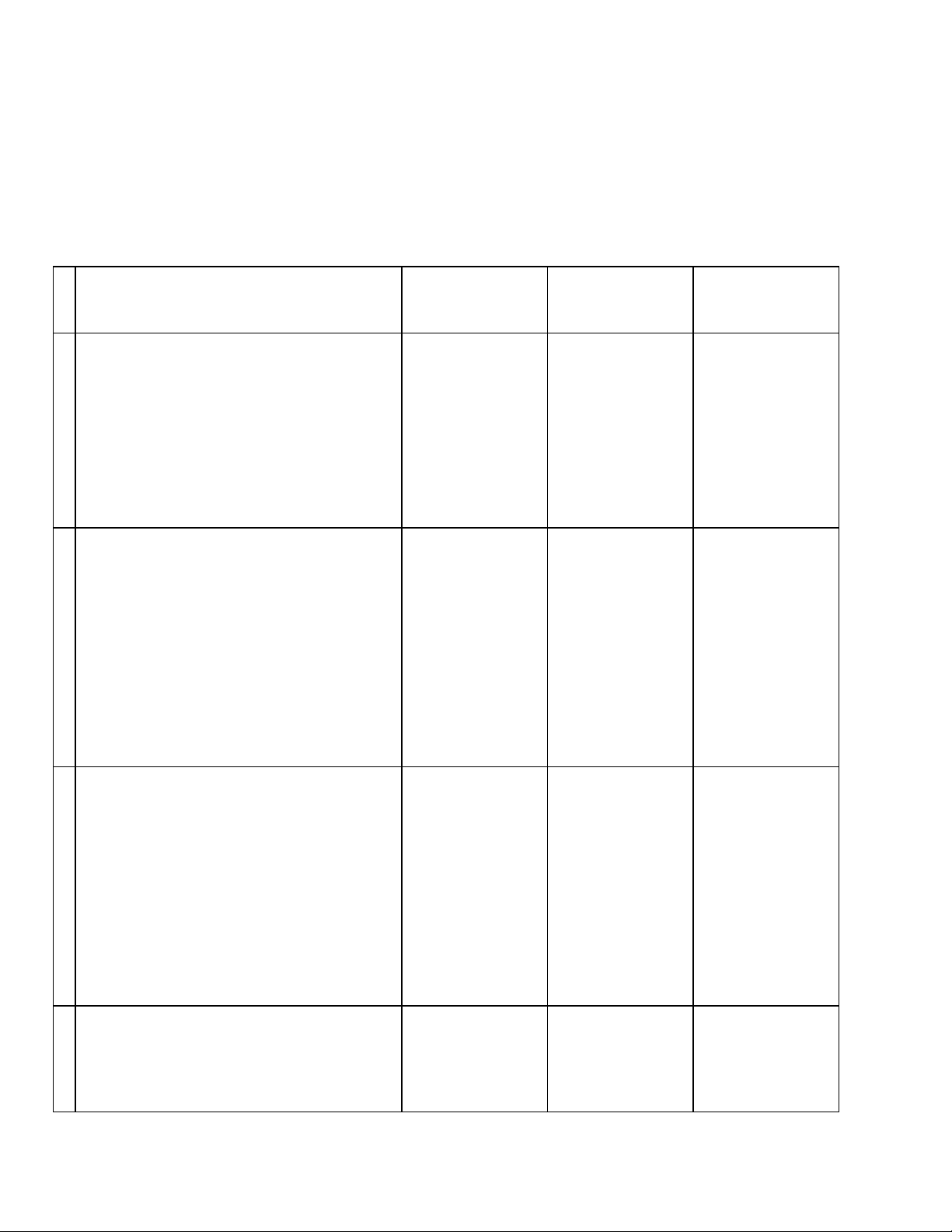

Visits (000s) by trip purpose 2019 and 2024

Trip purpose metrics 2019 and 2024

Business Holiday VFR Study Other

2019 4.2 6.0 9.0 42.1 6.2

2024 4.7 5.9 9.7 41.4 4.1

Change 0.5 -0.1 0.7 -0.7 -2.1

2019 £199 £162 £71 £71 £124

2024 £184 £160 £60 £62 £171

Change -£15 -£2 -£11 -£9 £47

2019 £834 £980 £640 £2,987 £768

2024 £867 £951 £579 £2,577 £694

Change £33 -£29 -£61 -£410 -£74

Average length

of stay (nights)

Average spend

per night at 2024

prices

Average spend

per visit at 2024

prices

Regional spread of inbound visits

Purpose mix of inbound visits (000s) by area in 2024

Change in inbound visits 2019-24 (000s)

Leading towns and cities for inbound holiday visits and spend in 2024

London 10,918 1£9,181 London

Edinburgh 1,769 2£1,225 Edinburgh

Manchester 462 3£236 Manchester

Liverpool 347 4£168 Liverpool

Glasgow 307 5£136 Oxford

Inverness 258 6£135 Inverness

Bath 206 7£132 Bath

Oxford 197 8£130 Glasgow

Brighton 174 9£111 Brighton

York 167 10 £75 Cardiff

Cardiff 147 11 £74 York

Bristol 141 12 £72 Cambridge

Birmingham 138 13 £67 Bristol

Cambridge 131 14 £63 Birmingham

Canterbury 121 15 £61 Canterbury

Leeds 82 16 £57 Chester

Stirling 81 17 £43 Southampton

Stratford-upon-Avon 77 18 £41 Stirling

Southampton 63 19 £35 Windsor

Chester 62 20 £32 Leeds

Source:ONS

Spend (£m)

Visits (000s)

Economics

Global population of High Net Worth Individuals in 2024 (millions and annual change)

At a global level the number of HNWIs

has increased by 30% since 2018

UK public sector debt as a percentage of GDP since 1993

Net interest payable on UK public sector debt (£m outturn prices, not seasonally adjusted)

The OBR forecast for 2025/26 is £111bn,

equivalent to about half annual spending on the

NHS and double the amount spent on defence

UK 30-year gilts: average monthly yield since 1998

Inflation vs Bank of England base rate

Price Indices for 12 months to Julyy 2025 (2015 = 100)

Holiday centres, camping sites, youth hostels and similar 193

Passenger transport by air 166

Travel insurance 163

Passenger transport by sea and inland waterway 163

Package holidays 155

Museums, libraries, zoological gardens 154

Hotels, motels and similar accomodation services 154

Restaurants and cafes 147

Toll facilities and parking meters 146

Passengar transport by taxi and hired car with driver 143

Recreational and sporting services: Attendance 142

Passenger transport by railway 139

Cinemas, theatres, concerts 137

Consumer Price Index 136

Petrol 122

Travel goods 94

Source; ONS

Exchange rates

If the US Supreme Court upholds the

view that Trump’s reciprocal tariffs are

illegal, global financial and currency

markets will likely be unsettled

Europe Brent Spot Price ($s per barrel, unadjusted for inflation)

OECD Consumer Confidence since 1973

Competitiveness

WEF analysis highlights price competitiveness as a key weakness (UK rank out of 119)

Some examples

Increased likelihood of a “visitor

levy” being introduced in parts of

England, Scotland and Wales

With the exception of those from

Ireland, visitors who don’t need a

visa are now required to apply for

an ETA, which will cost them £16

The most important drivers of destination choice for potential inbound visitors

Offers good value for money 66%

Is a welcoming place to visit 64%

Is good for relaxing, resting, recharging 61%

There is beautiful coast and countryside to explore 61%

I can roam around visiting many types of places 60%

It's easy to get around once there 60%

There is a good variety of food and drink to try 57%

It's easy to get to 55%

Is a place where I can explore history and heritage 54%

Offers lots of different experiences in one destination 54%

It has experiences I can't have anywhere else 53%

There are vibrant towns and cities to explore 53%

Is good for seeing famous sites, places, ticking off the 'must do' list 52%

Is inclusive and accessible for visitors like me 51%

Is good to visit at any time of year 50%

It has surprising and unexpected experiences 48%

Is a mixture of old and new 47%

Has an interesting mix of cultures from around the world 46%

There are interesting local people to meet 45%

It offers the opportunity to travel sustainably/responsibly 44%

Has a thriving arts and contemporary culture scene 41%

A good place for treating myself 40%

A place recommended by friends or family 40%

If I don't visit soon, I'd miss out 35%

Offers experiences I want to share on social media 34%

Findings based on research

undertaken by VisitBritain, with

percentages being the proportion

who scored each aspect as 5, 6 or 7

on a 7-point scale from “not at all

important” to “extremely important”

Proportion of potential visitors that associate Britain with each statement

Offers good value for money 33%

Is a welcoming place to visit 48%

Is good for relaxing, resting, recharging 38%

There is beautiful coast and countryside to explore 47%

I can roam around visiting many types of places 56%

It's easy to get around once there 53%

There is a good variety of food and drink to try 43%

Is easy to get to 48%

Is a place where I can explore history and heritage 57%

Offers lots of different experiences in one destination 53%

It has experiences I can't have anywhere else 44%

There are vibrant towns and cities to explore 57%

Is good for seeing famous sites, places, ticking off the 'must do' list 55%

Is inclusive and accessible for visitors like me 50%

Is good to visit at any time of year 42%

It has surprising and unexpected experiences 44%

Is a mixture of old and new 55%

Has an interesting mix of cultures from around the world 51%

There are interesting local people to meet 47%

It offers the opportunity to travel sustainably/responsibly 38%

Has a thriving arts and contemporary culture scene 47%

A good place for treating myself 40%

A place recommended by friends or family 39%

If I don't visit soon, I'd miss out 27%

Offers experiences I want to share on social media 42%

Perceptions of Britain around the world (Rank, typically out of fifty nations)

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

OVERALL Nations Brand Index 34433333333425645

Tourism 45544434534446666

Is rich in historic buildings and monuments 44445555555555555

Has a vibrant city life and urban attractions 44444444444446555

Would like to visit if money was no object 788666565656577710

Is rich in natural beauty 23 24 22 22 22 20 20 18 24 24 24 26 23 31 31 27 23

Culture 34644455554534345

Interesting & exciting contemporary culture 44443333434344444

Excels at sport 78856544545534555

Has a rich cultural heritage 67777776777768866

People 666444457667410 810 10

If visited, people would make me feel very welcome 14 13 13 12 13 10 13 11 12 13 15 16 11 18 16 19 18

Source: VisitBritain

Connectivity

Easy to reach

•There are few island nations that an international visitor can arrive at by sea,

rail or air

•Air is the mode of choice (or necessity) for the majority of international

visitors to Britain

•Focussing solely on scheduled air routes with more than 1,000 annual

passengers in 2024 the UK was connected to 110 countries and 403 foreign

airports

•Of the 1,781 distinct routes in operation 43% served an airport in or around

London

87% of inbound visitor spend comes courtesy of those visiting by air

By the end of the

decade Eurostar

should finally

face competition

Passenger mix by airport

Average daily flights at European airports (1st January-24th August 2025)

23rd Stansted 558

24th Manchester 553

37th Luton 371

40th Edinburgh 343

IST has 5 runways,

with a 6th by 2028,

AMS has 6 runways

Proportion of inbound holiday visitors using each mode to get around Britain

Public transport fares in Britain, most notably rail,

often compare unfavourably with those overseas,

especially for last minute purchases

The availability of public EV charging devices is highly variable (per 100,000 of population)

Demographics

Workforce age comparisons (Great Britain, 2023)

Projected population change in Great Britain over the next ten years

The cost of the state pension represented 2% of the economy

in the 1950s, today it’s 5%, by the 2070s it will be 8% if no

changes are made. The number of pensioners per 1,000

working age people is about 280 now, by 2070 it will be 393

Demographic change

•As is the case in Britain, an ageing population poses a challenge in many of

our European source markets

•In Asia, the demographic headwinds faced by Japan are well publicised, but

China faces an equally difficult predicament

•Migration is changing the profile of long-haul source markets such as

Australia, Canada and the USA, eroding how connected to Britain potential

visitors will feel

•Demand for accessible tourism is set to grow due to an ageing visitor profile

with additional needs, whether physical, sensory or cognitive

•This underscores the need to ensure that information, facilities and customer

service are as inclusive as is practical

QUESTIONS

Inbound tourism: the tailwinds and headwinds

David Edwards

September 2025

Context

Foreign bednights spent in Europe: 2014=100

Outbound travel from all world regions is forecast to grow this year and next

Intentions of Europeans to travel within Europe during next six months

Main challenges facing international tourism according to UNWTO Panel of Experts

Britain is being outcompeted in attracting inbound visitors (growth in period 1995-2024)

European destinations reporting inbound arrivals growth in first half of 2025

Across all countries to have reported

January to June figures to Tourmis

aggregate year-to-date growth in

foreign visitor arrivals stands at 5.1%

Inbound trends

Arrivals at the UK border – rolling 12-month tally

In the first half of 2025 the number of British National

arrivals is 7.2% up on the same period of last year, while

the number of Other Nationality arrivals is up just 0.6%

Visitor visas issued – rolling 12-month tally

In the first half of 2025 the number

of visitor visas issued was 5% up

on the same period of last year

Number of ETAs issued up to June 2025

Inbound volume and value trends 1980-2024

Volume remains 2% below 2019

and spend 8% down in real terms

Average spend per visit 1980-2024 (constant prices)

The amount that the typical inbound visit generates is now one-

third lower in real terms than had been the case in the mid 1980s

Average length of stay (nights) 1980-2024

The decline in spend per visit is due to

length of stay having fallen by around

one-third across the past four decades

Visits (000s) by trip purpose 2019 and 2024

Trip purpose metrics 2019 and 2024

Business Holiday VFR Study Other

2019 4.2 6.0 9.0 42.1 6.2

2024 4.7 5.9 9.7 41.4 4.1

Change 0.5 -0.1 0.7 -0.7 -2.1

2019 £199 £162 £71 £71 £124

2024 £184 £160 £60 £62 £171

Change -£15 -£2 -£11 -£9 £47

2019 £834 £980 £640 £2,987 £768

2024 £867 £951 £579 £2,577 £694

Change £33 -£29 -£61 -£410 -£74

Average length

of stay (nights)

Average spend

per night at 2024

prices

Average spend

per visit at 2024

prices

Regional spread of inbound visits

Purpose mix of inbound visits (000s) by area in 2024

Change in inbound visits 2019-24 (000s)

Leading towns and cities for inbound holiday visits and spend in 2024

London 10,918 1£9,181 London

Edinburgh 1,769 2£1,225 Edinburgh

Manchester 462 3£236 Manchester

Liverpool 347 4£168 Liverpool

Glasgow 307 5£136 Oxford

Inverness 258 6£135 Inverness

Bath 206 7£132 Bath

Oxford 197 8£130 Glasgow

Brighton 174 9£111 Brighton

York 167 10 £75 Cardiff

Cardiff 147 11 £74 York

Bristol 141 12 £72 Cambridge

Birmingham 138 13 £67 Bristol

Cambridge 131 14 £63 Birmingham

Canterbury 121 15 £61 Canterbury

Leeds 82 16 £57 Chester

Stirling 81 17 £43 Southampton

Stratford-upon-Avon 77 18 £41 Stirling

Southampton 63 19 £35 Windsor

Chester 62 20 £32 Leeds

Source:ONS

Spend (£m)

Visits (000s)

Economics

Global population of High Net Worth Individuals in 2024 (millions and annual change)

At a global level the number of HNWIs

has increased by 30% since 2018

UK public sector debt as a percentage of GDP since 1993

Net interest payable on UK public sector debt (£m outturn prices, not seasonally adjusted)

The OBR forecast for 2025/26 is £111bn,

equivalent to about half annual spending on the

NHS and double the amount spent on defence

UK 30-year gilts: average monthly yield since 1998

Inflation vs Bank of England base rate

Price Indices for 12 months to Julyy 2025 (2015 = 100)

Holiday centres, camping sites, youth hostels and similar 193

Passenger transport by air 166

Travel insurance 163

Passenger transport by sea and inland waterway 163

Package holidays 155

Museums, libraries, zoological gardens 154

Hotels, motels and similar accomodation services 154

Restaurants and cafes 147

Toll facilities and parking meters 146

Passengar transport by taxi and hired car with driver 143

Recreational and sporting services: Attendance 142

Passenger transport by railway 139

Cinemas, theatres, concerts 137

Consumer Price Index 136

Petrol 122

Travel goods 94

Source; ONS

Exchange rates

If the US Supreme Court upholds the

view that Trump’s reciprocal tariffs are

illegal, global financial and currency

markets will likely be unsettled

Europe Brent Spot Price ($s per barrel, unadjusted for inflation)

OECD Consumer Confidence since 1973

Competitiveness

WEF analysis highlights price competitiveness as a key weakness (UK rank out of 119)

Some examples

Increased likelihood of a “visitor

levy” being introduced in parts of

England, Scotland and Wales

With the exception of those from

Ireland, visitors who don’t need a

visa are now required to apply for

an ETA, which will cost them £16

The most important drivers of destination choice for potential inbound visitors

Offers good value for money 66%

Is a welcoming place to visit 64%

Is good for relaxing, resting, recharging 61%

There is beautiful coast and countryside to explore 61%

I can roam around visiting many types of places 60%

It's easy to get around once there 60%

There is a good variety of food and drink to try 57%

It's easy to get to 55%

Is a place where I can explore history and heritage 54%

Offers lots of different experiences in one destination 54%

It has experiences I can't have anywhere else 53%

There are vibrant towns and cities to explore 53%

Is good for seeing famous sites, places, ticking off the 'must do' list 52%

Is inclusive and accessible for visitors like me 51%

Is good to visit at any time of year 50%

It has surprising and unexpected experiences 48%

Is a mixture of old and new 47%

Has an interesting mix of cultures from around the world 46%

There are interesting local people to meet 45%

It offers the opportunity to travel sustainably/responsibly 44%

Has a thriving arts and contemporary culture scene 41%

A good place for treating myself 40%

A place recommended by friends or family 40%

If I don't visit soon, I'd miss out 35%

Offers experiences I want to share on social media 34%

Findings based on research

undertaken by VisitBritain, with

percentages being the proportion

who scored each aspect as 5, 6 or 7

on a 7-point scale from “not at all

important” to “extremely important”

Proportion of potential visitors that associate Britain with each statement

Offers good value for money 33%

Is a welcoming place to visit 48%

Is good for relaxing, resting, recharging 38%

There is beautiful coast and countryside to explore 47%

I can roam around visiting many types of places 56%

It's easy to get around once there 53%

There is a good variety of food and drink to try 43%

Is easy to get to 48%

Is a place where I can explore history and heritage 57%

Offers lots of different experiences in one destination 53%

It has experiences I can't have anywhere else 44%

There are vibrant towns and cities to explore 57%

Is good for seeing famous sites, places, ticking off the 'must do' list 55%

Is inclusive and accessible for visitors like me 50%

Is good to visit at any time of year 42%

It has surprising and unexpected experiences 44%

Is a mixture of old and new 55%

Has an interesting mix of cultures from around the world 51%

There are interesting local people to meet 47%

It offers the opportunity to travel sustainably/responsibly 38%

Has a thriving arts and contemporary culture scene 47%

A good place for treating myself 40%

A place recommended by friends or family 39%

If I don't visit soon, I'd miss out 27%

Offers experiences I want to share on social media 42%

Perceptions of Britain around the world (Rank, typically out of fifty nations)

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

OVERALL Nations Brand Index 34433333333425645

Tourism 45544434534446666

Is rich in historic buildings and monuments 44445555555555555

Has a vibrant city life and urban attractions 44444444444446555

Would like to visit if money was no object 788666565656577710

Is rich in natural beauty 23 24 22 22 22 20 20 18 24 24 24 26 23 31 31 27 23

Culture 34644455554534345

Interesting & exciting contemporary culture 44443333434344444

Excels at sport 78856544545534555

Has a rich cultural heritage 67777776777768866

People 666444457667410 810 10

If visited, people would make me feel very welcome 14 13 13 12 13 10 13 11 12 13 15 16 11 18 16 19 18

Source: VisitBritain

Connectivity

Easy to reach

•There are few island nations that an international visitor can arrive at by sea,

rail or air

•Air is the mode of choice (or necessity) for the majority of international

visitors to Britain

•Focussing solely on scheduled air routes with more than 1,000 annual

passengers in 2024 the UK was connected to 110 countries and 403 foreign

airports

•Of the 1,781 distinct routes in operation 43% served an airport in or around

London

87% of inbound visitor spend comes courtesy of those visiting by air

By the end of the

decade Eurostar

should finally

face competition

Passenger mix by airport

Average daily flights at European airports (1st January-24th August 2025)

23rd Stansted 558

24th Manchester 553

37th Luton 371

40th Edinburgh 343

IST has 5 runways,

with a 6th by 2028,

AMS has 6 runways

Proportion of inbound holiday visitors using each mode to get around Britain

Public transport fares in Britain, most notably rail,

often compare unfavourably with those overseas,

especially for last minute purchases

The availability of public EV charging devices is highly variable (per 100,000 of population)

Demographics

Workforce age comparisons (Great Britain, 2023)

Projected population change in Great Britain over the next ten years

The cost of the state pension represented 2% of the economy

in the 1950s, today it’s 5%, by the 2070s it will be 8% if no

changes are made. The number of pensioners per 1,000

working age people is about 280 now, by 2070 it will be 393

Demographic change

•As is the case in Britain, an ageing population poses a challenge in many of

our European source markets

•In Asia, the demographic headwinds faced by Japan are well publicised, but

China faces an equally difficult predicament

•Migration is changing the profile of long-haul source markets such as

Australia, Canada and the USA, eroding how connected to Britain potential

visitors will feel

•Demand for accessible tourism is set to grow due to an ageing visitor profile

with additional needs, whether physical, sensory or cognitive

•This underscores the need to ensure that information, facilities and customer

service are as inclusive as is practical

www.scatteredclouds.co.uk

@tourismstats.bsky.social

www.linkedin.com/in/scatteredclouds