Daiwa Capital Markets Flash: BYD (1211 HK) PDF Free Download

1 / 7/7

100%

See important disclosures, including any required research certifications, beginning on page 6

China

Consumer Discretionary

What’s new: We hosted a post-result NDR call with BYD management on

9 September 2024.

What’s the impact: 4m units sales volume target for 2024. BYD expects

2024 sales volume to hit 4m units (+33% YoY), driven by strong demand

for the DMi5 model seen in the domestic market. This is an upward revision

from its earlier target of 3.6m units (+20% YoY) set earlier this year.

Overseas market guidance is unchanged at 450,000-500,000 units for

2024 vs. 240,000 units in 2023. BYD’s sales volume for August 2024 was

371,000 units, up by 35% YoY. Management sees end-demand as stronger

than August sales volume, and believes the capacity and supply chain are

ready for higher sales volume in 2H24 vs. 1H24. We think monthly sales

volume could likely hit 440,000 units by December 2024, considering

management’s 4m guidance.

Overseas market strategy. YTD, Latin America sales grew the fastest,

followed by APAC and Europe. The introduction of the PHEV model this

year is an important driver for the overseas market. BYD is also expanding

into the Middle East and Africa. For 2025E, the earlier mentioned 1m units

overseas sales target can be a reference, but it will depend on end-demand

in 2H24. By region in 2025, BYD believes Latin America and APAC are

likely to contribute more than the EU. BYD sees the turning point in the EU

market in terms of sales will be when its Hungary factory is ready in late

2025. Currently, the major focus in Europe is to establish a presence. We

are upbeat on BYD’s global expansion story amid the global NEV transition

trend.

Profitability outlook. 2Q24 is the low point of the year due to the impact of

Honor version models, per BYD. From 3Q24, we believe the launch of the

DMi5 model is likely to be gross margin accretive, given its higher ASP. For

example, the Qin L (DMi5) price starts from CNY99,800 vs. Qin Honor’s

price of CNY79,800. We now look for 20% gross margin in 2H24E vs. 19%

in 2Q24.

What we recommend: We raise our 2024-26E EPS by 7-11% as we raise

our sales volume forecasts by 4-7% to 4.0-5.4m units to factor in

management’s sales volume guidance for 2024. We raise SOTP-based TP

to HKD376 from HKD351. We apply an unchanged 12x 2024-25E

EV/EBITDA multiple to the NEV business. Our TP implies a 20x 2025E

target PER. BYD currently trades at 13x 2025E PER, which is attractive in

our view. Key downside risk: lower-than-expected sales volume.

How we differ: Our 2024-26E EPS are 4-10% above the consensus likely

as we are more upbeat on its sales volume outlook.

9 September 2024

NDR takeaways: 4m sales volume target for 2024

➢ BYD expressed a positive view on volume and gross margin in 2H24

➢ Overseas guidance unchanged at 450,000-500,000 units for 2024

➢ Reaffirming our Buy (1) call; raising 12-month TP to HKD376

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

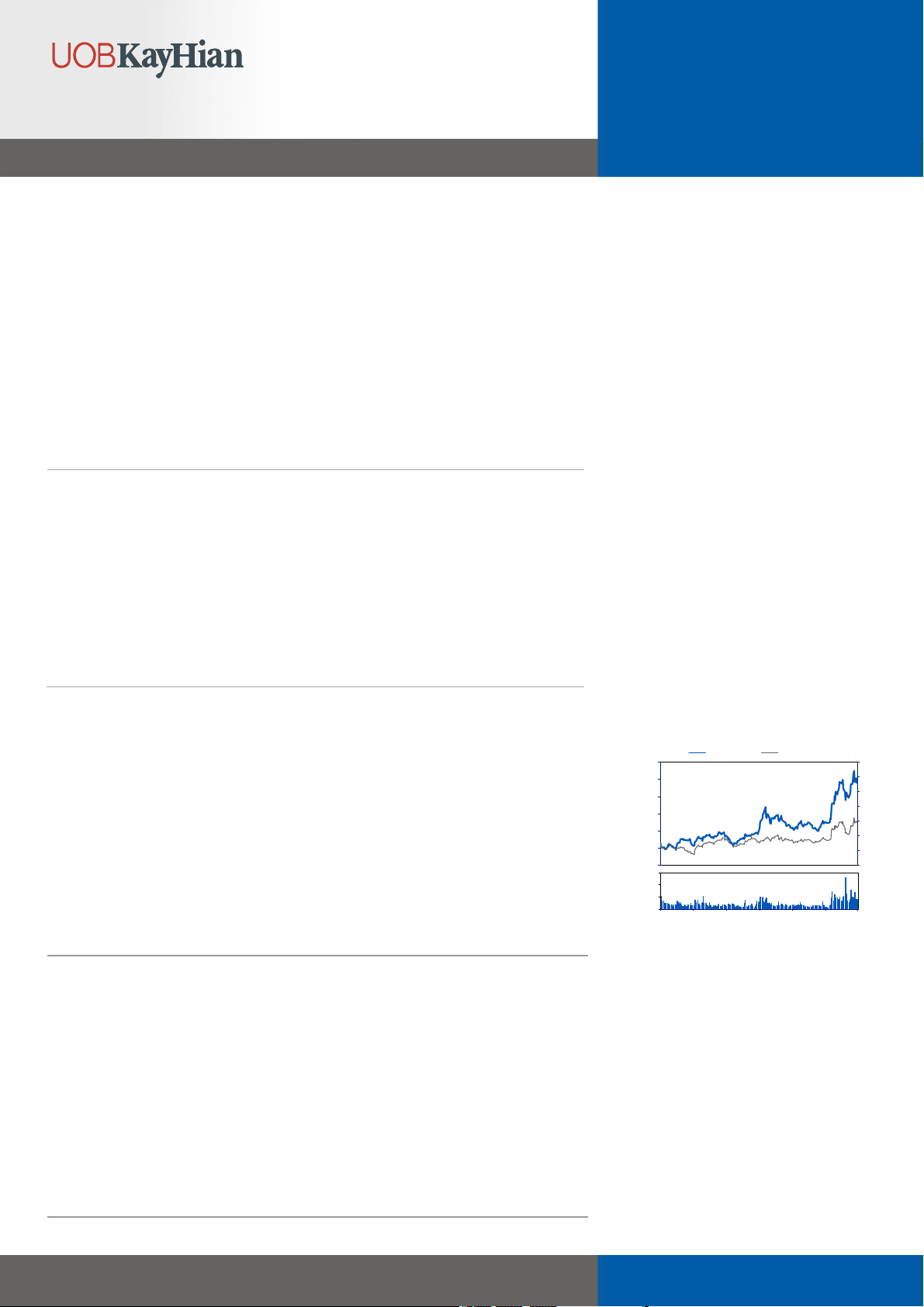

BYD (1211 HK)

Target price: HKD376.00(from HKD351.00)

Share price (9 Sep): HKD235.00 | Up/downside: +60.0%

Kelvin Lau

(852) 2848 4467

kelvin.lau@hk.daiwacm.com

Forecast revisions (%)

Year to 31 Dec 24E 25E 26E

Revenue change 5.3 14.1 21.5

Net profit change 7.0 9.5 11.4

Core EPS (FD) change 7.0 9.5 11.4

12-month range 171.70-257.40

Market cap (USDbn) 87.78

3m avg daily turnover (USDm) 173.76

Shares outstanding (m) 2,911

Major shareholder Mr. Wang Chuan-fu (17.6%)

Financial summary (CNY)

Year to 31 Dec 24E 25E 26E

Revenue (m) 741,865 906,626 1,048,177

Operating profit (m) 47,873 57,125 67,239

Net profit (m) 39,331 48,388 56,622

Core EPS (fully-diluted) 13.510 16.622 19.450

EPS change (%) 30.9 23.0 17.0

Daiwa vs Cons. EPS (%) 10.1 7.9 4.4

PER (x) 15.8 12.9 11.0

Dividend yield (%) 1.9 2.3 2.7

DPS 4.053 4.986 5.835

PBR (x) 3.7 3.0 2.5

EV/EBITDA (x) 5.8 4.8 3.2

ROE (%) 25.5 25.8 25.0

2

BYD (1211 HK): 9 September 2024

BYD: SOTP valuation

Multiple (x)

NAV 2024-25E

NAV

(CNY m)

per share

Mobile handset

10 x

122,681

42.1

Auto - NEV

12 x

976,338

335.4

Auto- EV Battery

20 x

28,800

9.9

Sub-total

1,127,818

387.4

- Net debt/cash

117,460

40.3

- Minority interest

(13,311)

(4.6)

Equity value (CNY m)

1,231,967

423.2

Exchange rate, 1HKD = x CNY

0.90

Equity value (HKD mn)

1,368,852

Conglomerate discount

20%

Equity value/share (HKD)

376.00

Source: Daiwa

3

BYD (1211 HK): 9 September 2024

Financial summary

Key assumptions

Profit and loss (CNYm)

Cash flow (CNYm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2019 2020 2021 2022 2023 2024E 2025E 2026E

BYD NEV volume (units) 229,506 189,689 603,783 1,863,494 3,024,417 3,966,400 4,814,600 5,414,600

Volume growth - NEV (%) (7.4) (17.3) 218.3 208.6 62.3 31.1 21.4 12.5

BYD NEV ASP (CNY) 111,381 125,861 144,740 165,000 151,200 139,104 146,059 153,362

ASP growth - NEV (%) (12.6) 13.0 15.0 14.0 (8.4) (8.0) 5.0 5.0

Year to 31 Dec 2019 2020 2021 2022 2023 2024E 2025E 2026E

Automobile 55,537 76,958 128,960 315,691 470,853 561,158 712,471 839,487

Mobile handset 52,522 59,354 86,454 98,815 118,577 166,008 179,454 193,990

Other Revenue 13,719 17,157 727 9,554 12,885 14,700 14,700 14,700

Total Revenue 121,778 153,469 216,142 424,061 602,315 741,865 906,626 1,048,177

Other income 2,019 (340) (1,963) (7,796) (8,606) (9,793) (11,242) (10,901)

COGS (103,702) (126,226) (187,998) (351,816) (480,558) (592,209) (726,743) (842,159)

SG&A (14,208) (16,916) (19,783) (43,722) (78,248) (91,991) (111,515) (127,878)

Other op.expenses 0 0 0 0 0 0 0 0

Operating profit 5,887 9,988 6,399 20,727 34,903 47,873 57,125 67,239

Net-interest inc./(exp.) (3,134) (2,909) (1,276) 513 969 197 404 267

Assoc/forex/extraord./others (322) (196) (605) (160) 1,397 2,209 2,209 2,209

Pre-tax profit 2,431 6,883 4,518 21,080 37,269 50,278 59,739 69,715

Tax (312) (869) (551) (3,367) (5,925) (9,289) (9,558) (11,154)

Min. int./pref. div./others (504) (1,780) (922) (1,091) (1,303) (1,659) (1,793) (1,938)

Net profit (reported) 1,614 4,234 3,045 16,622 30,041 39,331 48,388 56,622

Net profit (adjusted) 1,614 4,234 3,045 16,622 30,041 39,331 48,388 56,622

EPS (reported)(CNY) 0.592 1.552 1.080 5.710 10.319 13.510 16.622 19.450

EPS (adjusted)(CNY) 0.592 1.552 1.080 5.710 10.319 13.510 16.622 19.450

EPS (adjusted fully-diluted)(CNY) 0.592 1.552 1.080 5.710 10.319 13.510 16.622 19.450

DPS (CNY) 0.060 0.155 0.105 1.142 3.096 4.053 4.986 5.835

EBIT 5,887 9,988 6,399 20,727 34,903 47,873 57,125 67,239

EBITDA 15,358 22,178 20,064 41,097 78,454 84,344 101,482 119,552

Year to 31 Dec 2019 2020 2021 2022 2023 2024E 2025E 2026E

Profit before tax 2,431 6,883 4,518 21,080 37,269 50,278 59,739 69,715

Depreciation and amortisation 9,471 12,190 13,665 20,370 43,553 36,471 44,356 52,313

Tax paid (445) (449) (254) 0 0 (9,289) (9,558) (11,154)

Change in working capital (5,757) 11,743 41,940 98,418 92,494 72,533 22,996 112,565

Other operational CF items 9,041 15,026 5,598 970 (3,591) (13) (473) (473)

Cash flow from operations 14,741 45,393 65,467 140,838 169,725 149,981 117,059 222,965

Capex (20,627) (11,774) (37,344) (108,030) (124,177) (99,526) (96,479) (98,627)

Net (acquisitions)/disposals (505) (1,268) (1,847) 12,803 22,245 0 0 0

Other investing CF items 251 (1,402) (6,213) (25,370) (23,732) 0 0 0

Cash flow from investing (20,881) (14,444) (45,404) (120,596) (125,664) (99,526) (96,479) (98,627)

Change in debt 7,179 (19,291) (13,006) (16,413) 18,073 (8,600) 0 0

Net share issues/(repurchases) 0 0 0 0 0 0 0 0

Dividends paid (948) (441) (671) 0 0 (9,012) (11,799) (14,516)

Other financing CF items 379 (9,174) 29,740 (3,076) (5,256) (2,196) (1,736) (1,736)

Cash flow from financing 6,610 (28,907) 16,063 (19,489) 12,817 (19,808) (13,535) (16,252)

Forex effect/others 0 0 0 0 0 0 0 0

Change in cash 470 2,041 36,125 753 56,879 30,646 7,046 108,086

Free cash flow (5,886) 33,619 28,123 32,808 45,548 50,455 20,581 124,338

4

BYD (1211 HK): 9 September 2024

Financial summary continued …

Balance sheet (CNYm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2019 2020 2021 2022 2023 2024E 2025E 2026E

Cash & short-term investment 11,674 13,738 49,820 51,182 108,512 139,158 146,204 254,290

Inventory 25,572 31,396 43,355 79,107 87,677 108,047 132,593 153,650

Accounts receivable 40,135 39,308 35,593 38,828 61,866 59,349 90,663 83,854

Other current assets 29,586 27,162 37,342 71,685 44,067 46,958 50,372 53,305

Total current assets 106,967 111,605 166,110 240,804 302,121 353,513 419,831 545,099

Fixed assets 55,296 58,202 75,545 176,502 265,630 317,652 359,249 395,596

Goodwill & intangibles 11,954 10,174 10,116 23,289 41,664 52,697 63,222 73,189

Other non-current assets 21,425 21,037 44,009 53,265 70,132 72,342 74,551 76,760

Total assets 195,642 201,017 295,780 493,861 679,548 796,203 916,853 1,090,645

Short-term debt 54,062 27,645 22,939 5,153 18,323 10,323 10,323 10,323

Accounts payable 35,341 49,792 79,044 143,766 198,483 236,884 254,360 328,442

Other current liabilities 18,626 28,994 69,321 184,426 236,860 291,738 356,530 412,195

Total current liabilities 108,029 106,431 171,304 333,345 453,667 538,945 621,214 750,961

Long-term debt 21,916 23,626 10,790 7,594 11,975 11,375 11,375 11,375

Other non-current liabilities 3,095 6,507 9,442 31,533 63,444 63,444 63,444 63,444

Total liabilities 133,040 136,563 191,536 372,471 529,086 613,764 696,032 825,779

Share capital 2,728 2,728 2,911 2,911 2,911 2,911 2,911 2,911

Reserves/R.E./others 54,034 54,146 92,159 108,118 135,899 166,217 202,806 244,912

Shareholders' equity 56,762 56,874 95,070 111,029 138,810 169,129 205,717 247,823

Minority interests 5,839 7,580 9,175 10,361 11,652 13,311 15,104 17,042

Total equity & liabilities 195,642 201,017 295,780 493,861 679,548 796,203 916,853 1,090,645

EV 688,269 661,832 607,365 574,207 532,650 492,853 485,391 377,034

Net debt/(cash) 64,304 37,532 (16,091) (38,436) (78,213) (117,460) (124,505) (232,592)

BVPS (CNY) 20.806 20.847 32.657 38.139 47.682 58.097 70.665 85.129

Year to 31 Dec 2019 2020 2021 2022 2023 2024E 2025E 2026E

Sales (YoY) (0.0) 26.0 40.8 96.2 42.0 23.2 22.2 15.6

EBITDA (YoY) (8.3) 44.4 (9.5) 104.8 90.9 7.5 20.3 17.8

Operating profit (YoY) (21.1) 69.7 (35.9) 223.9 68.4 37.2 19.3 17.7

Net profit (YoY) (41.9) 162.3 (28.1) 445.9 80.7 30.9 23.0 17.0

Core EPS (fully-diluted) (YoY) (41.9) 162.3 (30.4) 428.7 80.7 30.9 23.0 17.0

Gross-profit margin 14.8 17.8 13.0 17.0 20.2 20.2 19.8 19.7

EBITDA margin 12.6 14.5 9.3 9.7 13.0 11.4 11.2 11.4

Operating-profit margin 4.8 6.5 3.0 4.9 5.8 6.5 6.3 6.4

Net profit margin 1.3 2.8 1.4 3.9 5.0 5.3 5.3 5.4

ROAE 2.9 7.5 4.0 16.1 24.0 25.5 25.8 25.0

ROAA 0.8 2.1 1.2 4.2 5.1 5.3 5.6 5.6

ROCE 4.5 7.9 5.0 15.2 22.2 24.9 25.6 25.4

ROIC 4.3 7.6 5.9 20.4 37.8 56.9 59.5 87.8

Net debt to equity 113.3 66.0 net cash net cash net cash net cash net cash net cash

Effective tax rate 12.8 12.6 12.2 16.0 15.9 18.5 16.0 16.0

Accounts receivable (days) 126.4 94.5 63.2 32.0 30.5 29.8 30.2 30.4

Current ratio (x) 1.0 1.0 1.0 0.7 0.7 0.7 0.7 0.7

Net interest cover (x) 1.9 3.4 5.0 n.a. n.a. n.a. n.a. n.a.

Net dividend payout 10.1 10.0 9.7 20.0 30.0 30.0 30.0 30.0

Free cash flow yield n.a. 5.4 4.5 5.3 7.3 8.1 3.3 20.0

Company profile

Listed in Hong Kong in 2002, BYD is engaged in the R&D, manufacture and distribution of automobiles,

rechargeable batteries and mobile phone components. It owns 65% of BYD Electronics (285 HK, Not

rated). BYD focuses on autos (especially NEVs), rechargeable batteries (lithium-ion and nickel batteries

used in mobile phones and other portable electronic devices), as well as mobile-phone components and

its mobile phones assembly business (casings, keypads, mobile-phone designs, etc.).

5

BYD (1211 HK): 9 September 2024

ESG analysis

Source: Daiwa, Company

ESG opportunities

Opportunities Management Analyst comments

EGreen technology 1

Continuous breakthroughs in technology allow BYD to deliver more environmentally-friendly,

high-performance products, such as its DM-i model. Fuel consumption for the DM-i is 4L/100km

vs. 7L/100km for ICEs. We expect strong demand for its DM-i model, leading to strong YoY

growth in BYD's auto sales going forward.

ESG risks

Risks Management Analyst comments

G

Executive/board

quality 2BYD’s board has 6 directors, 3 of whom are independent. Among the directors, Mr. Chuanfu

Wang also serves as the company's CEO.

Capital management 2 BYD paid a dividend of CNY3.1 per share in 2023, representing a dividend payout ratio of 30%.

Related party &

transaction 2Sales to related parties accounted for 0.4% of total 2023 revenue, while purchases from related

parties constituted 3% of the cost of sales.

SProduct quality &

safety 1

BYD was one of the first vehicle manufacturers to implement a 'quality system competitiveness

index' and to create the role of development quality engineers to monitor the quality of its

products.

SProduct design &

lifecycle management 2The company has a strong product design capacity given the high level of fuel efficacy of its DMi

PHEV models (close to 4L/100) and the innovative development of its blade LFP batteries.

EMaterials sourcing &

efficiency 2

BYD sources key components and parts from industry-leading suppliers. It has also formed a

'green supplier, green material' system to ensure that external sources meet its environmental

standards. For its battery business, BYD has its own cathode capacity, which we believe helps

improve its operational efficiency.

Note: Management score represents a company's ability to

manage/benefit from

certain

ESG

topics. The scores range

from 1

to

3,

with

1

being the strongest.

Last update: 19 Jun 2024

6

BYD (1211 HK): 9 September 2024

Important Disclosures and Disclaimer

This publication is produced by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, and distributed by Daiwa Securities Group Inc. and/or its non-U.S. affiliates, except to the extent expressly

provided herein. This publication and the contents hereof are intended for information purposes only, and may be subject to change without further notice. Any use, disclosure, distribution,

dissemination, copying, printing or reliance on this publication for any other purpose without our prior consent or approval is strictly prohibited. Neither Daiwa Securities Group Inc. nor any of its

respective parent, holding, subsidiaries or affiliates, nor any of its respective directors, officers, servants and employees, represent nor warrant the accuracy or completeness of the information

contained herein or as to the existence of other facts which might be significant, and will not accept any responsibility or liability whatsoever for any use of or reliance upon this publication or any

of the contents hereof. Neither this publication, nor any content hereof, constitute, or are to be construed as, an offer or solicitation of an offer to buy or sell any of the securities or investments

mentioned herein in any country or jurisdiction nor, unless expressly provided, any recommendation or investment opinion or advice. Any view, recommendation, opinion or advice expressed in

this publication may not necessarily reflect those of Daiwa Securities Group Inc., and/or its affiliates nor any of its respective directors, officers, servants and employees except where the publication

states otherwise. This research report is not to be relied upon by any person in making any investment decision or otherwise advising with respect to, or dealing in, the securities mentioned, as it

does not take into account the specific investment objectives, financial situation and particular needs of any person.

Daiwa Securities Group Inc., its subsidiaries or affiliates, or its or their respective directors, officers and employees from time to time have trades as principals, or have positions in, or have other

interests in the securities of the company under research including market making activities, derivatives in respect of such securities or may have also performed investment banking and other

services for the issuer of such securities. Daiwa Securities Group Inc., its subsidiaries or affiliates do and seek to do business with the company(s) covered in this research report. Therefore,

investors should be aware that a conflict of interest may exist. The following are additional disclosures.

Ownership of Securities

For “Ownership of Securities” information, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationship

For “Investment Banking Relationship”, please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Daiwa Securities Co. Ltd. and Daiwa Securities Group Inc.

Daiwa Securities Co. Ltd. is a subsidiary of Daiwa Securities Group Inc.

Investment Banking Relationship

Within the preceding 12 months, the subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has lead-managed public offerings and/or secondary offerings of the equities or relevant Within

the preceding 12 months, Daiwa Capital Markets Hong Kong Limited has lead-managed public offerings and/or secondary offerings of the equities or relevant securities of the following companies:

Neusoft Xikang Holdings Inc (9686 HK), Luyuan Group Holding (Cayman) Limited (2451 HK) and Vingroup Joint Stock Company (VIC VN).

*Subsidiaries of Daiwa Securities Group Inc. for the purposes of this section shall mean any one or more of: Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司), Daiwa Capital

Markets Singapore Limited, Daiwa Capital Markets Australia Limited, Daiwa-Cathay Capital Markets Co., Ltd., Daiwa Securities Capital Markets Korea Co., Ltd.

Within the last 12 months, the subsidiaries and/or affiliates of Daiwa Securities Group Inc. * has received compensation for investment banking services from CSC Financial Co Ltd (6066 HK),

Kanzhun Ltd (2076 HK/BZ US), Lotte Tour Development Co Ltd (032350 KS), Daiwa Securities Group Inc (8601 JP), Senko Group Holdings Co Ltd (9069 JP) and Lotte Rental Co Ltd (089860 KS).

Hong Kong

This research is distributed in Hong Kong by Daiwa Capital Markets Hong Kong Limited (大和資本市場香港有限公司) (“DHK”) which is regulated by the Hong Kong Securities and Futures

Commission. Recipients of this research in Hong Kong may contact DHK in respect of any matter arising from or in connection with this research.

Investment Banking Relationship

Within the preceding 12 months, Daiwa Capital Markets Hong Kong Limited has lead-managed public offerings and/or secondary offerings of the equities or relevant securities of the following

companies: Neusoft Xikang Holdings Inc (9686 HK), Luyuan Group Holding (Cayman) Limited (2451 HK) and Vingroup Joint Stock Company (VIC VN).

Within the preceding 12 months, Daiwa Capital Markets Hong Kong Limited has received compensation for investment banking services from Kanzhun Ltd (2076 HK).

Relevant Relationship (DHK)

DHK may from time to time have an individual employed by or associated with it serves as an officer of any of the companies under its research coverage.

Singapore

This research is distributed in Singapore by Daiwa Capital Markets Singapore Limited and it may only be distributed in Singapore to accredited investors, expert investors and institutional investors

as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. By virtue of distribution to these category of investors, Daiwa

Capital Markets Singapore Limited and its representatives are not required to comply with Section 36 of the Financial Advisers Act (Chapter 110) (Section 36 relates to disclosure of Daiwa Capital

Markets Singapore Limited’s interest and/or its representative’s interest in securities). Recipients of this research in Singapore may contact Daiwa Capital Markets Singapore Limited in respect of

any matter arising from or in connection with the research.

Australia

This research is distributed in Australia by Daiwa Capital Markets Australia Limited and it may only be distributed in Australia to wholesale investors within the meaning of the Corporations Act.

Recipients of this research in Australia may contact Daiwa Capital Markets Stockbroking Limited in respect of any matter arising from or in connection with the research.

Taiwan

This research is solely for reference and not intended to provide tailored investment recommendations. This research is distributed in Taiwan by Daiwa-Cathay Capital Markets Co., Ltd. and it

may only be distributed in Taiwan to specific customers who have signed recommendation contracts with Daiwa-Cathay Capital Markets Co., Ltd. and non-customers including (i) professional

institutional investors, (ii) TWSE or TPEx listed companies, upstream and downstream vendors, and specialists that offer or seek advice, and (iii) potential customers with an actual need for

business development in accordance with the Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. Recipients of this research including non-

customer recipients of this research shall not provide it to others or engage in any activities in connection with this research which may involve conflicts of interests. Neither Daiwa-Cathay Capital

Markets Co., Ltd. nor its personnel who writes or reviews the research report has any conflict of interest in this research. Since Daiwa-Cathay Capital Markets Co., Ltd. does not operate brokerage

trading business in foreign markets, this research is prepared on a “without recommendation” to any foreign securities basis and Daiwa-Cathay Capital Markets Co., Ltd. does not accept

orders from customers to trade in such foreign securities. Recipients of this research shall carefully judge their own investment risk and take full responsibility for the results of any resulting

investments in the companies and/or sectors featured in this research. Without the prior written permission of Daiwa-Cathay Capital Markets Co., Ltd., recipients of this research are prohibited

from disclosing the research to the media, reprinting the research, or quoting from the research to other parties. Recipients of this research in Taiwan may contact Daiwa-Cathay Capital Markets

Co., Ltd. in respect of any matter arising from or in connection with the research.

Thailand

This research is distributed to only institutional investors in Thailand. This report is provided to you for informational purposes only. Information contained herein is not intended to be, and shall not

be construed as, an offer or an invitation for subscription or purchase of securities in Thailand. This document has not been and will not be registered with, or approved by, the Office of the

Securities and Exchange Commission of Thailand. As neither Daiwa Securities Group Inc. nor any of its subsidiaries or affiliates, nor any of the foregoing entities’ respective directors, officers,

servants and employees are licensed to carry on any securities business in Thailand, this document is intended to be read by the addressee who is an institutional investor only and may not be

circulated or distributed, whether directly or indirectly, to the public or any members of the public in Thailand, unless to the extent permitted by applicable laws and regulations.

This report is prepared by analysts who are employed by Daiwa Securities Group Inc. and/or its non-U.S. affiliates. Neither Daiwa Securities Group Inc. nor any of its subsidiaries or affiliates, nor

any of the foregoing entities’ respective directors, officers, servants and employees accept any liability whatsoever for any direct or consequential loss arising from any use of this research or its

contents.

The information and opinions contained herein have been compiled or arrived at from sources believed to be reliable. However, neither Daiwa Securities Group Inc. nor any of its subsidiaries or

affiliates, nor any of the foregoing entities’ respective directors, officers, servants and employees make any representation or warranty, express or implied, as to their accuracy or completeness.

Expressions of opinion herein are subject to change without notice. The use of any information, forecasts and opinions contained in this report shall be at the sole discretion and risk of the user.

Daiwa Securities Group Inc., its subsidiaries and affiliates and their respective directors, officers, servants and employees may have positions and financial interest in securities mentioned in this

research. Daiwa Securities Group Inc. and its subsidiaries and affiliates may from time to time perform investment banking or other services for, or solicit investment banking or other business

from, any entity mentioned in this research. Therefore, investors should be aware of conflict of interest that may affect the objectivity of this research.

United Kingdom

These materials constitute independent research for the purposes of the Financial Conduct Authority (“FCA”) Conduct of Business Rules. These materials have been produced by Daiwa Securities

Co. Ltd (“DSCL”) and/or its affiliates and are distributed by Daiwa Capital Markets Europe Limited (“DCME”) to persons classified as (i) eligible counterparties; and (ii) professional clients for the

purposes of the Conduct of Business Rules of the FCA. These materials should not be disseminated to any retail clients in the United Kingdom. DCME is authorised and regulated by the FCA and

is a member of the London Stock Exchange. DCME’s FCA registration number is 124490 and the FCA's registered address is 25 The North Colonnade, London, E14 5HS.

DCME makes no representation as to the completeness, accuracy or timeliness of any of the materials produced by DSCL, and does not accept any liability for any losses, costs, liabilities or

expenses which may arise directly or indirectly from any use of, or reliance on the materials.

DCME and/or its affiliates may, from time to time, to the extent permitted by law, participate or invest in, or be mandated in respect of transactions with the issuer(s) referred to in the materials

prepared by DSCL, perform services for or solicit business from such issuers, and/or have a position or effect transactions in a particular issuer’s securities and/or may have acted as an underwriter

during the past twelve months in respect of a particular issuer of its securities. DCME does not review DSCL’s materials prior to publication on DCME’s platforms and has no influence over its

content. DCME has in place organisational arrangements for the prevention and avoidance of conflicts of interest, including information barriers to control the flow of information between the private

and public sides of the firm. A summary of DCME’s conflict management policies are available at http://www.uk.daiwacm.com/about-us/corporate-governance-regulatory.

DSCL’s materials are distributed by DCME only as permitted by law. The materials are not directed to, or intended for distribution to or use by, any person or entity located in any jurisdiction where

7

BYD (1211 HK): 9 September 2024

such distribution, publication, availability or use would be contrary to law or regulation or would subject DCME to any regulation or licensing requirement within such jurisdiction.

Germany

Research reports are produced by Daiwa Securities Co. Ltd. and/or its affiliates and are distributed by Daiwa Capital Markets Deutschland GmbH in the European Union. Daiwa Capital Markets

Deutschland GmbH is authorised and regulated by Bundesanstalt für Finanzdienstleistungsaufsicht (“BaFin“) under the reference number 149361. Daiwa Capital Markets Deutschland GmbH and

its affiliates may, from time to time, to the extent permitted by law, participate or invest in, or be mandated in respect of, other financing transactions with the issuer(s) of the securities referred to

herein (the “Securities”), perform services for or solicit business from such issuers, and/or have a position or effect transactions in the Securities or options thereof.

This publication is intended for investors who are Professional Clients or Eligible Counterparties in the European Union within the meaning of Directive 2014/65/EU (“MiFID II”) and should therefore

not be distributed to Retail Clients in the European Union.

Daiwa Capital Markets Deutschland GmbH has in place organisational arrangements for the identification, prevention and management of conflicts of interest. Information regarding our conflict

management are available at: https://www.de.daiwacm.com/policies/

Additional disclosures regarding specific company names and related financial instruments are available at: https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Bahrain

This research material is distributed in Bahrain by Daiwa Capital Markets Europe Limited, Bahrain Branch, regulated by The Central Bank of Bahrain and holds Investment Business Firm – Category

2 license and having its official place of business at the Bahrain World Trade Centre, South Tower, 7th floor, P.O. Box 30069, Manama, Kingdom of Bahrain. Tel No. +973 17534452 Fax No. +973

535113

United States

This research is distributed into the United States directly by Daiwa Capital Markets Hong Kong Limited (DCMHK) and in certain cases indirectly by Daiwa Capital Markets America Inc. (DCMA),

a U.S. Securities and Exchange Commission registered broker-dealer and FINRA member firm, exclusively to “major U.S. institutional investors”, as defined under Rule 15a-6 promulgated under

the U.S. Securities Exchange Act of 1934, as amended, and as interpreted by the staff of the U.S. Securities and Exchange Commission (SEC). Where this is co-branded research published by

Daiwa’s partners in collaboration with other parties not affiliated with Daiwa, this research is distributed in the United States by DCMHK only. This report is not an offer to sell or the solicitation of

any offer to buy securities. U.S. customers wishing to effect transactions in any designated investment discussed in this report should do so through a qualified salesperson of DCMA. Non-U.S.

customers wishing to effect transactions in any designated investment discussed in this report should contact a Daiwa entity in their local jurisdiction. The securities or other investment products

discussed in this report may not be eligible for sale in some jurisdictions.

Analysts employed outside the U.S., as specifically indicated elsewhere in this report, are not registered as research analysts with FINRA. These analysts may not be associated persons of DCMA,

and therefore may not be subject to FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

ADDITIONAL IMPORTANT DISCLOSURES CAN BE FOUND AT:

https://daiwa3.bluematrix.com/sellside/Disclosures.action

Ownership of Securities

For “Ownership of Securities” information please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Investment Banking Relationships

For “Investment Banking Relationships” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

DCMA Market Making

For “DCMA Market Making” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action.

Research Analyst Conflicts

For updates on “Research Analyst Conflicts” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The principal research analysts who prepared this

report have no financial interest in securities of the issuers covered in the report, are not (nor are any members of their household) an officer, director or advisory board member of the issuer(s)

covered in the report, and are not aware of any material relevant conflict of interest involving the analyst or DCMA, and did not receive any compensation from the issuer during the past 12 months

except as noted: no exceptions.

Research Analyst Certification

For updates on “Research Analyst Certification” and “Rating System” please visit BlueMatrix disclosure link at https://daiwa3.bluematrix.com/sellside/Disclosures.action. The views about any and

all of the subject securities and issuers expressed in this Research Report accurately reflect the personal views of the research analyst(s) primarily responsible for this report (or the views of the

firm producing the report if no individual analyst is named on the report); and no part of the compensation of such analyst (or no part of the compensation of the firm if no individual analyst is named

on the report) was, is, or will be directly or indirectly related to the specific recommendations or views contained in this Research Report.

The following explains the rating system in the report as compared to relevant local indices, unless otherwise stated, based on the beliefs of the author of the report.

"1": the security could outperform the local index by more than 15% over the next 12 months.

"2": the security is expected to outperform the local index by 5-15% over the next 12 months.

"3": the security is expected to perform within 5% of the local index (better or worse) over the next 12 months.

"4": the security is expected to underperform the local index by 5-15% over the next 12 months.

"5": the security could underperform the local index by more than 15% over the next 12 months.

Disclosure of investment ratings

Rating

Percentage of total

Buy*

74.13%

Hold**

19.13%

Sell***

6.74%

Source: Daiwa

Notes: data is for single-branded Daiwa research in Asia (ex Japan) and correct as of 30 June 2024.

* comprised of Daiwa’s Buy and Outperform ratings.

** comprised of Daiwa’s Hold ratings.

*** comprised of Daiwa’s Underperform and Sell ratings.

Additional information may be available upon request.

Japan - additional notification items pursuant to Article 37 of the Financial Instruments and Exchange Law

(This Notification is only applicable where report is distributed by Daiwa Securities Co. Ltd.)

If you decide to enter into a business arrangement with us based on the information described in materials presented along with this document, we ask you to pay close attention to the following

items.

• In addition to the purchase price of a financial instrument, we will collect a trading commission* for each transaction as agreed beforehand with you. Since commissions may be included in the

purchase price or may not be charged for certain transactions, we recommend that you confirm the commission for each transaction.

• In some cases, we may also charge a maximum of ¥ 2 million (including tax) per year as a standing proxy fee for our deposit of your securities, if you are a non-resident of Japan.

• For derivative and margin transactions etc., we may require collateral or margin requirements in accordance with an agreement made beforehand with you. Ordinarily in such cases, the amount

of the transaction will be in excess of the required collateral or margin requirements.

• There is a risk that you will incur losses on your transactions due to changes in the market price of financial instruments based on fluctuations in interest rates, exchange rates, stock prices,

real estate prices, commodity prices, and others. In addition, depending on the content of the transaction, the loss could exceed the amount of the collateral or margin requirements.

• There may be a difference between bid price etc. and ask price etc. of OTC derivatives handled by us.

• Before engaging in any trading, please thoroughly confirm accounting and tax treatments regarding your trading in financial instruments with such experts as certified public accountants.

*The amount of the trading commission cannot be stated here in advance because it will be determined between our company and you based on current market conditions and the content of

each transaction etc.

When making an actual transaction, please be sure to carefully read the materials presented to you prior to the execution of agreement, and to take responsibility for your own decisions regarding

the signing of the agreement with us.

Corporate Name: Daiwa Securities Co. Ltd.

Financial instruments firm: chief of Kanto Local Finance Bureau (Kin-sho) No.108

Memberships: Japan Securities Dealers Association, The Financial Futures Association of Japan,

Japan Securities Investment Advisers Association, Type II Financial Instruments Firms Association,

Japan Security Token Offering Association