Global Energy Transition Trends PDF Free Download

1 / 24/24

100%

Global Energy

Transition Trends

Green Energy Export Day 2025,

Copenhagen

Oliver Metcalfe

August 27, 2025

1Global Trends in Clean Power

BNEF coverage

2Global Trends in Clean Power

Source: Getty Images.

3Global Trends in Clean Power

1. Investment and deployment

“Different directions”

4Global Trends in Clean Power

Source: BloombergNEF. Note: Start years differ by sector but all sectors are present from 2020 onward. Most notably, nuclear figures start in 2015 and power grids in

2020. CCS refers to carbon capture and storage.

Global investment in energy transition, by sector

Global energy transition investment

exceeded $2 trillion for the first time

33 51 80 108 135 152 231 285 260 238 341 383 426 456 518 576

929

1,177

1,517

1,881

2,083

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

$ billion

Power grids

Clean industry

Electrified heat

Clean shipping

Electrified transport

Hydrogen

CCS

Nuclear

Energy storage

Renewable energy

Clean

energy

Transport

Buildings

Industry

Grids

AMER +7%

EMEA -1.7%

APAC +21%

Global Change +10.7%

5Global Trends in Clean Power

Source: BloombergNEF. Note: CCS refers to carbon capture and storage.

Energy transition investment trends: “mature” sectors Energy transition investment trends: “emerging” sectors

Energy transition investment trends

diverged by sector maturity

815

1,043

1,357

1,683

1,929

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2020 2021 2022 2023 2024

$ billion

Power

grids

Electrified

transport

Energy

storage

Renewable

energy

+14.7%

93% of total investment

114

134

160

199

154

0

100

200

300

2020 2021 2022 2023 2024

$ billion

Clean

industry

Electrified

heat

Clean

shipping

Hydrogen

CCS

Nuclear

-23%

7% of total investment

6Global Trends in Clean Power

Source: BloombergNEF

Global cumulative renewable energy capacity, historic and forecast to 2035

…but still falls short of what’s needed

for a net-zero pathway

Net Zero Scenario

0

5

10

15

20

25

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Terawatts

Other renewables Onshore wind Offshore wind Utility-scale solar Residential solar

Commercial solar Solar buffer Energy storage Pumped hydro

7Global Trends in Clean Power

Source: BloombergNEF. Note: 'Others' includes biomass and waste, small hydro and marine.

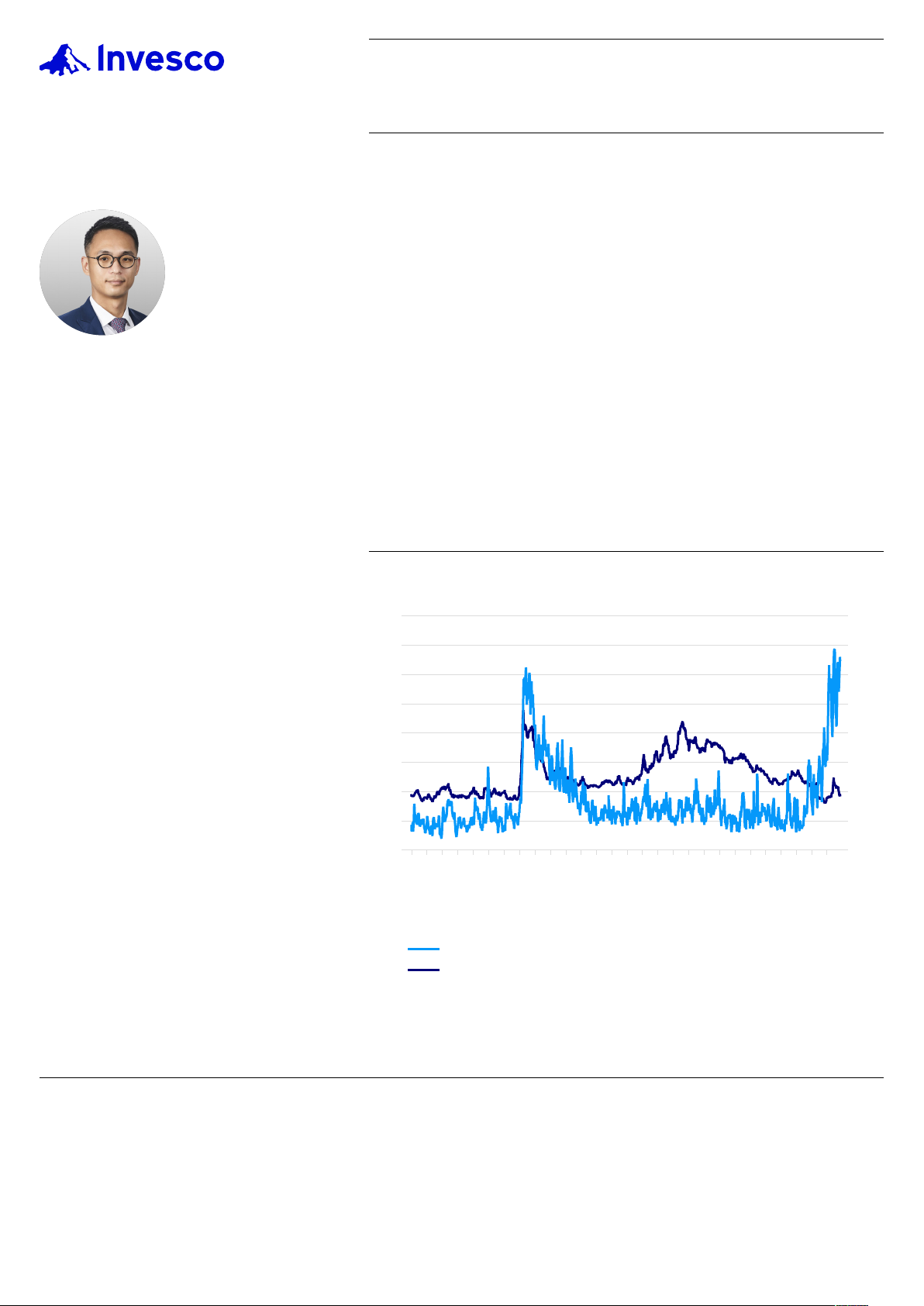

Global biannual investment in renewable energy

Onshore wind and utility-scale solar

shrink as small-scale solar grows

0

100

200

300

400

500

1H 2004

2H 2004

1H 2005

2H 2005

1H 2006

2H 2006

1H 2007

2H 2007

1H 2008

2H 2008

1H 2009

2H 2009

1H 2010

2H 2010

1H 2011

2H 2011

1H 2012

2H 2012

1H 2013

2H 2013

1H 2014

2H 2014

1H 2015

2H 2015

1H 2016

2H 2016

1H 2017

2H 2017

1H 2018

2H 2018

1H 2019

2H 2019

1H 2020

2H 2020

1H 2021

2H 2021

1H 2022

2H 2022

1H 2023

2H 2023

1H 2024

2H 2024

1H 2025

$ billion

Solar Wind Co-located Biofuels Geothermal Others

8Global Trends in Clean Power

Source: BloombergNEF. Note: 'Others' includes biomass and waste, small hydro and marine.

Global biannual investment in renewable energy

Onshore wind and utility-scale solar

shrink as small-scale solar grows

0

100

200

300

400

500

1H 2004

2H 2004

1H 2005

2H 2005

1H 2006

2H 2006

1H 2007

2H 2007

1H 2008

2H 2008

1H 2009

2H 2009

1H 2010

2H 2010

1H 2011

2H 2011

1H 2012

2H 2012

1H 2013

2H 2013

1H 2014

2H 2014

1H 2015

2H 2015

1H 2016

2H 2016

1H 2017

2H 2017

1H 2018

2H 2018

1H 2019

2H 2019

1H 2020

2H 2020

1H 2021

2H 2021

1H 2022

2H 2022

1H 2023

2H 2023

1H 2024

2H 2024

1H 2025

$ billion

Small-scale solar Utility-scale solar Onshore wind Offshore wind Co-located Biofuels Geothermal Others

9Global Trends in Clean Power

Source: BloombergNEF, PV Infolink. Note: Values shown for a market without major trade barriers, such as Europe, mainland China and Latin America. Modules are

bifacial TOPCon modules. W(DC) is watts (direct current).

Capex benchmark for medium-sized fixed-axis utility-scale PV projects, historical and forecast

Solar module prices fall to record-low

of 9.2 US cents per watt

2.44 1.85

1.22 1.00 0.88 0.84 0.55 0.48 0.34 0.30 0.28 0.28 0.20 0.16 0.10 0.09

4.34

3.57

2.33 2.10 1.91 1.85

1.44 1.31 1.09 1.03 0.81 0.73 0.64 0.62 0.52 0.50

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Module Balance of plant and inverter Engineering, procurement and construction Other

2023 $/W(DC)

10 Global Trends in Clean Power

Source: BloombergNEF. Note: LCOE is levelized cost of electricity. Offshore wind includes offshore transmission costs. The global benchmarks are capacity-

weighted averages. LCOEs do not include subsidies or tax-credits. MWh is megawatt-hour.

Impact of mainland China on global wind LCOE benchmarks

Wind cost divide has widened between

mainland China market and rest of world

38

87 87

57

89

121

44

30

86

59

2021 2022 2023 2024

$/MWh (nominal)

Global benchmark Rest of World China benchmark

Mainland China benchmark

11 Global Trends in Clean Power

Source: BloombergNEF. Note: CCS refers to carbon capture and storage.

Energy transition investment trends: “mature” sectors Energy transition investment trends: “emerging” sectors

Energy transition investment trends

diverged by sector maturity

815

1,043

1,357

1,683

1,929

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2020 2021 2022 2023 2024

$ billion

Power

grids

Electrified

transport

Energy

storage

Renewable

energy

+14.7%

93% of total investment

114

134

160

199

154

0

100

200

300

2020 2021 2022 2023 2024

$ billion

Clean

industry

Electrified

heat

Clean

shipping

Hydrogen

CCS

Nuclear

-23%

7% of total investment

12 Global Trends in Clean Power

Finding a buyer willing to sign a binding

offtake agreement is even harder

Source: BloombergNEF. Note: Data as of October 31, 2024. BNEF’s Hydrogen Offtake Agreement Database only includes projects of over 20 megawatts or 2,800

metric tons/year of capacity. Pre-contractual agreements include term sheets, letters of intent (LOI), and heads of agreements.

Clean H2 offtake by agreement type

Offtaker identified, 6%

Offtaker not identified, 94%

12%

21%

16%

30%

21%

0%

20%

40%

60%

80%

100%

All announced supply Capacity with offtaker identified

Share of total capacity, share of offtake capacity

Unspecified

Memorandum of understanding

Pre-contractual agreement

Self consumption

Binding offtake

13 Global Trends in Clean Power

2. Data centers

“Ramping up

demand”

14 Global Trends in Clean Power

Source: BloombergNEF. Note: Data-center demand refers to total energy demand. BNEF’s Economic Transition Scenario combines near-term market analysis, least-

cost modeling, consumer adoption trends, and historical patterns to project how commercially available technologies are likely to scale. It assumes no new policy

interventions and is designed to reveal the economic fundamentals driving the energy transition.

Data centers will add as much power

demand as EVs in the coming decade

Average hourly US data-center electricity demand

0

50

100

150

200

250

300

350

400

2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Terawatt-hours

Data centers

Electric vehicles

Industry

15 Global Trends in Clean Power

Source: BloombergNEF, Lawrence Berkeley National Lab (LBNL) , International Energy Agency (IEA) 2024 , Boston Consulting Group (BCG) , Electric Power

Research Institute (EPRI) , Jefferies, Goldman Sachs, McKinsey, S&P, IEA 2025. Note: The data underlying the above forecasts include both published figures and

BloombergNEF estimates, derived from visuals in third-party reports using chart extraction software and data interpolation methods. All sources are cited and linked

in the report. Derived estimates represent the independent interpretation of BloombergNEF and do not imply endorsement by the original data providers.

BNEF’s estimates are less bullish than

some others

Comparison of US data-center energy demand forecasts

0

100

200

300

400

500

600

700

800

900

1,000

1,100

2014 2016 2018 2020 2022 2024 2026 2028 2030

TWh BCG

S&P

McKinsey

Jeffries

IEA 2025

LBNL historical

LBNL high

LBNL low

IEA

Goldman Sachs

EPRI historical

EPRI higher

EPRI high

EPRI moderate

EPRI low

BNEF

16 Global Trends in Clean Power

3. Tariffs

“Reshoring, rewiring,

and bewildering”

17 Global Trends in Clean Power

Source: BloombergNEF, Bloomberg, The Wall Street Journal, The New York Times, The Economist, The Guardian

Tariff uncertainty

18 Global Trends in Clean Power

Source: BloombergNEF. Note: Includes factory investment across the manufacture of solar (polysilicon, wafers, cells and modules), batteries (separators,

electrolytes, cathodes, anodes and cells), wind turbines (nacelles only), and hydrogen electrolyzer manufacturing (stack assembly only). Manufacturing capacity has

been risk-adjusted to account for the likelihood of completion and factory ramp up according to such factors as factory location, manufacturer experience, and

capacity of the plant. ‘Other’ refers to rest of world, and ‘Other East Asia’ comprises Taiwan, Japan and South Korea.

Clean-tech factory investment growing

outside mainland China

Clean-tech factory investment by geography

12

21 25

43

59

125

102

126

108

95

0

20

40

60

80

100

120

140

2018 2019 2020 2021 2022 2023 2024 2025e 2026e 2027e

$ billion

Mainland China

US

Europe

India

Southeast Asia

Other East Asia

Other

Risk-adjusted outlook

19 Global Trends in Clean Power

Source: BloombergNEF. Note: Includes factory investment across the manufacture of solar (polysilicon, wafers, cells and modules), batteries (separators,

electrolytes, cathodes, anodes and cells), wind turbines (nacelles only), and hydrogen electrolyzer manufacturing (stack assembly only). Manufacturing capacity has

been risk-adjusted to account for the likelihood of completion and factory ramp-up according to such factors as factory location, manufacturer experience, and

capacity of the plant.

Batteries dominate factory investment

Global clean-tech factory investment by technology

12

21 25

43

59

125

102

126

108

95

0

20

40

60

80

100

120

140

2018 2019 2020 2021 2022 2023 2024 2025e 2026e 2027e

$ billion

Hydrogen

Wind

Solar

Batteries

Risk-adjusted outlook

20 Global Trends in Clean Power

China’s clean-tech exports increasingly

heading to low-to-mid income countries

Source: BloombergNEF, Sinoimex. Note: Income country group classification by the World Bank according to gross national income per capita for 2024.

Chinese clean-tech exports by value, technology and income group of destination country

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2024

2022

2024

2022

2024

2022

2024

2022

2024

2022

Wind

turbines

Solar

modules

Plug-in

hybrids

Electric

vehicles

Lithium-

ion

batteries

Low-to-upper-middle income High income

Lithium-ion batteries

Electric vehicles

Plug-in hybrid vehicles

Solar modules

Wind turbines

21 Global Trends in Clean Power

Source: Getty Images.

22 Global Trends in Clean Power

Copyright

© Bloomberg Finance L.P. 2025. This publication is the copyright of Bloomberg Finance L.P. in connection with BloombergNEF. No portion of this document may be

photocopied, reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of BloombergNEF.

Disclaimer

The BloombergNEF ("BNEF"), service/information is derived from selected public sources. Bloomberg Finance L.P. and its affiliates, in providing the

service/information, believe that the information it uses comes from reliable sources, but do not guarantee the accuracy or completeness of this information, which is

subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements in this service/document reflect the current

judgement of the authors of the relevant articles or features, and do not necessarily reflect the opinion of Bloomberg Finance L.P., Bloomberg L.P. or any of their

affiliates (“Bloomberg”). Bloomberg disclaims any liability arising from use of this document, its contents and/or this service. Nothing herein shall constitute or be

construed as an offering of financial instruments or as investment advice or recommendations by Bloomberg of an investment or other strategy (e.g., whether or not

to “buy”, “sell”, or “hold” an investment). The information available through this service is not based on consideration of a subscriber's individual circumstances and

should not be considered as information sufficient upon which to base an investment decision. You should determine on your own whether you agree with the

content. This service should not be construed as tax or accounting advice or as a service designed to facilitate any subscriber's compliance with its tax, accounting or

other legal obligations. Employees involved in this service may hold positions in the companies mentioned in the services/information.

The data included in these materials are for illustrative purposes only. The BLOOMBERG TERMINAL service and Bloomberg data products (the “Services”) are

owned and distributed by Bloomberg Finance L.P. (“BFLP”) except (i) in Argentina, Australia and certain jurisdictions in the Pacific islands, Bermuda, China, India,

Japan, Korea and New Zealand, where Bloomberg L.P. and its subsidiaries (“BLP”) distribute these products, and (ii) in Singapore and the jurisdictions serviced by

Bloomberg's Singapore office, where a subsidiary of BFLP distributes these products. BLP provides BFLP and its subsidiaries with global marketing and operational

support and service. Certain features, functions, products and services are available only to sophisticated investors and only where permitted. BFLP, BLP and their

affiliates do not guarantee the accuracy of prices or other information in the Services. Nothing in the Services shall constitute or be construed as an offering of

financial instruments by BFLP, BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or

whether or not to “buy”, “sell” or “hold” an investment. Information available via the Services should not be considered as information sufficient upon which to base an

investment decision. Bloomberg makes no claims or representations, or provides any assurances, about the sustainability characteristics, profile or data points of any

underlying issuers, products or services, and users should make their own determination on such issues. The following are trademarks and service marks of BFLP, a

Delaware limited partnership, or its subsidiaries: BLOOMBERG, BLOOMBERG ANYWHERE, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG

PROFESSIONAL, BLOOMBERG TERMINAL and BLOOMBERG.COM. Absence of any trademark or service mark from this list does not waive Bloomberg's

intellectual property rights in that name, mark or logo. All rights reserved. © 2025 Bloomberg.

Copyright and disclaimer

BloombergNEF (BNEF) is a strategic

research provider covering global commodity

markets and the disruptive technologies

driving the transition to a low-carbon

economy.

Our expert coverage assesses pathways for

the power, transport, industry, buildings and

agriculture sectors to adapt to the energy

transition.

We help commodity trading, corporate

strategy, finance and policy professionals

navigate change and generate opportunities.

<Help>

support.bnef@bloomberg.net

Client enquiries:

Bloomberg Terminal: press <Help> key twice

Email: support.bnef@bloomberg.net

Learn more:

about.bnef.com | @BloombergNEF

Oliver Metcalfe

ometcalfe@bloomberg.net