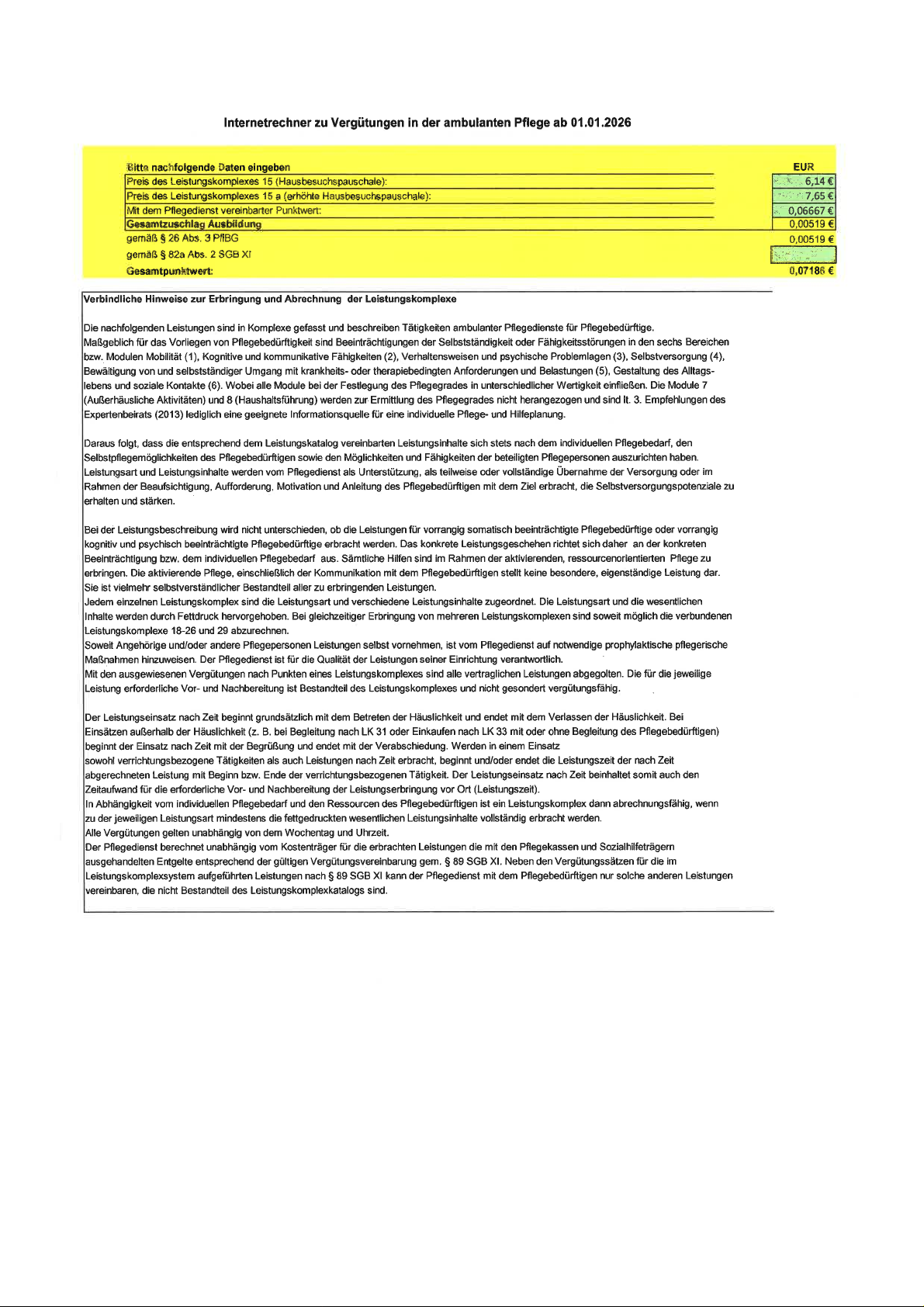

Truckload Market Overview PDF Free Download

1 / 33/33

100%

©DAT Freight & Analytics

Truckload Market

Overview

May 2025

Dean Croke, Principal Analyst

©DAT Freight & Analytics

Dia l-A-Truck

First Load Board

©DAT Freight & Analytics

•Demand Indicator: brokers & carriers benefiting from tariff-related volume surge -up 9% y/y and 10% vs long-term average

for Week 18. Shippers are urgently seeking bonded storage, free trade zones, and overflow warehouse space to avoid

tariffs.

•Dry van loads moved in April were 6% higher than the busiest week during the pandemic -Nov 12, 2021

•Spot Rates: produce seasonality starting to lift spot rates off the bottom of the April trough.

•Flatbed spot rates are strong as seasonality demand drives higher volumes during of building, planting, construction

and nursery seasons. Spot rates up 8% y/y, but forecast to peak 6/2 at +$0.17c higher y/y

•Contract Rates: treading water. Dry van new rates (NRD) entering routing guides up slightly. Reefer/Flatbed still negative.

•Spot Market Capacity: grew in April -highest number of for-hire authorities in two years. Market favors IC’s

•Small Fleet/Owner-Operator Profitability: Falling falling diesel prices not enough to offset decreasing spot rates. Carrier

gross profit margin drops from -$0.04/mile in April to -$0.07/mile below breakeven, same as last April.

•Produce Season: down 8% y/y or 2,000 fewer truckloads after a late start to the season. California down 27% y/y (11,264

few TL YTD) after a cooler March/April. Reefer truck availability (2) the lowest since May 2019 during the freight recession.

State of the Market Summary

3

©DAT Freight & Analytics

Broker Trends

4

©DAT Freight & Analytics

Broker Authorities

5

●Total active broker authorities down

10% y/y and 1% m/m in April.

●At 23,956, broker authorities are

still 14% higher than April 2020,

right as the pandemic started.

●Net loss of 153 broker authorities in

April.

●26% fewer brokers since the Oct ‘22

peak.

●New broker authorities in April were

37% lower than last year.

©DAT Freight & Analytics

Truckload Capacity

Trends

6

©DAT Freight & Analytics

Large Fleet Capacity -Quarterly Changes

7

●Large fleet truck counts end Q125

down 1% q/q and 5% y/y

●Down 20% from the mid-2022

peak reading of 93.

●Large fleets have been decreasing

fleet size for 12 quarters

○Slashed counts for 9 quarters

○Trimmed over the last 3

●The slowing rate of declines

suggests large carriers are still

uncertain about future demand.

●New Class 8 truck orders in April

down 52% y/y. ACT Research

carrier profitability fell to levels not

seen since Q1 2010.

TCI measures truck capacity at large, publicly traded trucking companies on a quarterly basis using end-of-quarter truck counts reported

within their earnings statements. Indexed to 100 during the 4th quarter in 2006.

©DAT Freight & Analytics

Interstate Truckload Capacity -Monthly Changes

8

●Small fleet capacity turns positive for the

second month in April as the most new

carriers enter the market in 2 years.

●New carrier authorities jumped by 48%

m/m and 30% y/y.

●Compared to the pre-pandemic April

average (highlighted), last months new

entrant levels were 49% higher.

●Carrier exits were 26% higher in April

compared to March, the highest in 12

months.

●Net change -+971 carriers.

Note : Th is d a t a a p p lie s to a ll ve h ic le s in v o lve d in in te rs ta te c o m m e r c e o ve r 10 ,0 0 0 lb s GVW.

©DAT Freight & Analytics

Independent Owner-Operator Cost Dynamics

9

●Small fleet profitability deteriorated in

April to -$0.07/mile gross profit margin

following January’s boost (+$0.06/mile GP)

in rates from the extreme cold.

●Carrier profit margins are about the same

as April last year.

●Last two years -losing on average

$0.02/mile

●Carrier operating costs averaged

$1.77/mile in April on the back of lower

diesel costs (31% of costs / $0.54/mile):

○down $0.14/mile (4%) in the last month

○$0.39/mile (10%) in the last year.

©DAT Freight & Analytics

Independent Owner-Operator vs Leased-On

10

©DAT Freight & Analytics

Demand Trends

11

©DAT Freight & Analytics

U.S. Co n ta in e riz e d Im p o rts

12

●April 2025 import volumes as measured

by TEU Volume (twenty-foot equivalent

units), were down 0.7% month-over-

month (m/m) but up 14.4% year-over-

year (y/y), and the second-highest ever

recorded for April.

●Many shippers have been front-loading

cargo to avoid peak season surcharges,

potential disruption associated with ILA

strike action, tariffs and Red Sea

diversions.

●Current volume is 24% higher than the

long-term April average or the equivalent

of 188,516 truckloads (2.6 TEU:1 TL ratio)

©DAT Freight & Analytics

U.S. Co n ta in e riz e d Im p o rts Fa ll-Off

13

●Container vessels arrivals down 20% in May

●33 container ship “blank sailings” will skip LA

or Long Beach 6 May –20 June.

©DAT Freight & Analytics

Truckload Demand -TTMI

14

●The February Trucking Ton-Mile Index

(TTMI) indicates freight demand

improved by almost 1%, regaining the

loss from the prior month (due to the

extreme cold weather).

●TTMI was flat compared to last year.

●Regarding absolute demand levels,

trucking demand is:

○1.5% higher than Feb 2018

○1.6% higher than Feb 2019

○1.8% higher than Feb 2020.

2018

2019

TTMI is calculated as a weighted geometric mean for 41 freight-generating sectors across food, chemical manufacturing, mining, paper,

aggregates, wholesaling, retailing, and warehousing.

Feb ‘22

Pandemic

Feb ‘18

Feb ‘19

©DAT Freight & Analytics

ISM PMI

15

●US ISM Manufacturing PMI dropped

to a 5-month low in April of 48.70.

●The second straight monthly decline

in the PMI ended a brief recovery in

manufacturing.

●The April ISM PMI data on

manufacturing new orders, improved

by 7.7% m/m but down 0.8% y/y.

●Readings of of a PMI > 55 are what

we would consider favorable to

truckload

R-value 0.91

©DAT Freight & Analytics

Produce Season -Week Ending 4/29

16

•North American truckload produce volumes

end April 8% lower y/y:

○US (56%) -12% lower y/y

○Canada (6%) -up 4% y/y

○Mexico (37%) -down 4% y/y

•After a late start due to cooler weather,

California is 27% lower y/y:

○11,264 fewer truckloads YTD

•Florida is 15% lower y/y

©DAT Freight & Analytics

Spot Rate Trends

17

©DAT Freight & Analytics

Spot / Contract Load Mix

18

10 Year Average

Equipment Type Contract Spot

Dry Van 86% 14%

Reefer 87% 13%

Flatbed 73% 27%

March 2025

●83% Contract

●17 % S p o t

March 2025

●60 % Contract

●40% Spot

March 2025

●86% Contract

●14 % S p o t

©DAT Freight & Analytics

Rate Trends -Dry Va n

19

●Dry van linehaul rates decreased by almost $0.02/mile

last week to a national average of $1.60/mile on a 1%

lower volume of loads moved. At $1.60/mile, linehaul

rates remained $0.03/mile higher than last year and

almost identical to 2024.

●On DAT's Top 50 lanes, ranked by the volume of loads

moved, carriers were paid an average of $1.89/mile,

down a penny-per-mile and $0.29/mile higher than the

national 7-day rolling average spot rate.

●In our Midwest Region bellwether states (n=13), which

account for 45% of loads moved nationally last week

and have the highest correlation to the national

average, outbound spot rates were down $0.02/mile

on a 1% lower volume of outbound loads moved.

○Carriers were paid an average of $1.72/mile,

$0.12/mile higher than the national 7-day

rolling average.

©DAT Freight & Analytics

Se a s o n a lity Tre n d s -Dry Va n

20

©DAT Freight & Analytics

Spot Rate Trends -Dry Va n

21

S p o t lin e h a ul ra t e s n e g a tiv e y / y fo r 2 7

months

The last spot market cycle ran from June ‘20 to June ‘24 (49 months) -22 months of extreme expansion & 27 months of contraction. Now 8 months +ve

©DAT Freight & Analytics

Rate Trends -Reefer

22

●Available reefer capacity loosened slightly

last week, with the national average

reefer spot rate ending the week at

$1.91/mile, down almost a penny per

mile.

●Reefer spot rates are $0.02/mile lower

than last year and $0.05/mile lower than

2023.

●Peak floral shipments drove up spot rates

in Miami; outbound reefer spot rates

were the highest in three years, up

$0.54/mile to $2.43/mile last week on a

28% higher w/w volume.

●The high-volume lane from Miami to

Atlanta paid carriers an average of

$2.84/mile, up $1.33/mile or 88% in the

last month.

©DAT Freight & Analytics

Se a s o n a lity Tre n d s -Reefer

23

©DAT Freight & Analytics

Rate Trends -Reefer

24

S p o t lin e h a ul ra t e s n e g a tiv e y / y fo r 2 7

months

©DAT Freight & Analytics

Rate Trends -Fla tb e d

25

●After being flat the week prior,

flatbed spot rates decreased by just

over a penny per mile last week,

averaging $2.15/mile on a 2% lower

volume of loads moved.

●Compared to last year, the flatbed

7-day rolling average is $0.13/mile

higher, $0.02/mile higher than

2023, but $0.21/mile lower than

the flatbed bull market in 2018.

©DAT Freight & Analytics

Se a s o n a lity Tre n d s -Fla tb e d

26

©DAT Freight & Analytics

Rate Trends -Fla tb e d

27

©DAT Freight & Analytics

Two Data Points

to Watch

28

©DAT Freight & Analytics

©2022 DAT Freight & Analytics, LLC. Company Confidential.

29

Dry Van Contract New Rate Development

Dry Van NRD for May 15:

●Active rates down 0.2% (-0.4%)

●Replacement rates down 0.9%

(+2.2%)

●This means that new contract rates

are almost 1% lower than the rates

being replaced.

●Was in positive territory for almost

a year after decreasing for almost

three years.

●But….are barely above parity for the

last 12 months (average +0.2%)

©DAT Freight & Analytics

©2022 DAT Freight & Analytics, LLC. Company Confidential.

30

Reefer New Rate Development

Reefer NRD for May 15th:

●Active rates down 1.2% (-1.5%)

●Replacement rates down 0.1%

(+0.8%)

●This means that new contract rates

are almost much the same as the

rates being replaced.

●But….are slightly below parity for

the last 12 months (average -1.3%)

©DAT Freight & Analytics

©2022 DAT Freight & Analytics, LLC. Company Confidential.

31

Flatbed New Rate Development

Flatbed NRD for May 15th:

●Active rates down 0.4%

(+2.6%)

●Replacement rates down

3.0% (-6.4%)

●This means that new contract

rates are 3.0% below the

rates being replaced.

●But….are significantly below

parity for the last 12 months

(average -4.8%).

©DAT Freight & Analytics

Intermodal Spot Rates

32

Intermodal and Dry Van TL Spot Rates

●Intermodal plays a critical role in identifying the

strength of market changes because it offers

shippers an essential outlet for additional 53’

capacity during periods of tight truckload

supply.

●When intermodal spot rates (5% of volume)

begin to rise meaningfully along with increasing

truckload rates, it’s a strong indicator that

we’re seeing a true market turnaround.

●While there have been minor fluctuations

recently in spot rates, they lack the consistency

and breadth needed to drive a sustained

increase.

●Both have been moving sideways for the past 9

months. Current spread is $0.44/mile vs 12-

month average spread of $0.48/mile

●Since April 2024, intermodal spot rates have

dropped by 5.3%; dry van rates ex FSC are

mostly flat.

©DAT Freight & Analytics

Thank You.